(Un) Stable Coins and (De) Centralisation

What happens when Stable Coins go bust, and Decentralised finance isn't actually what it seems to be?

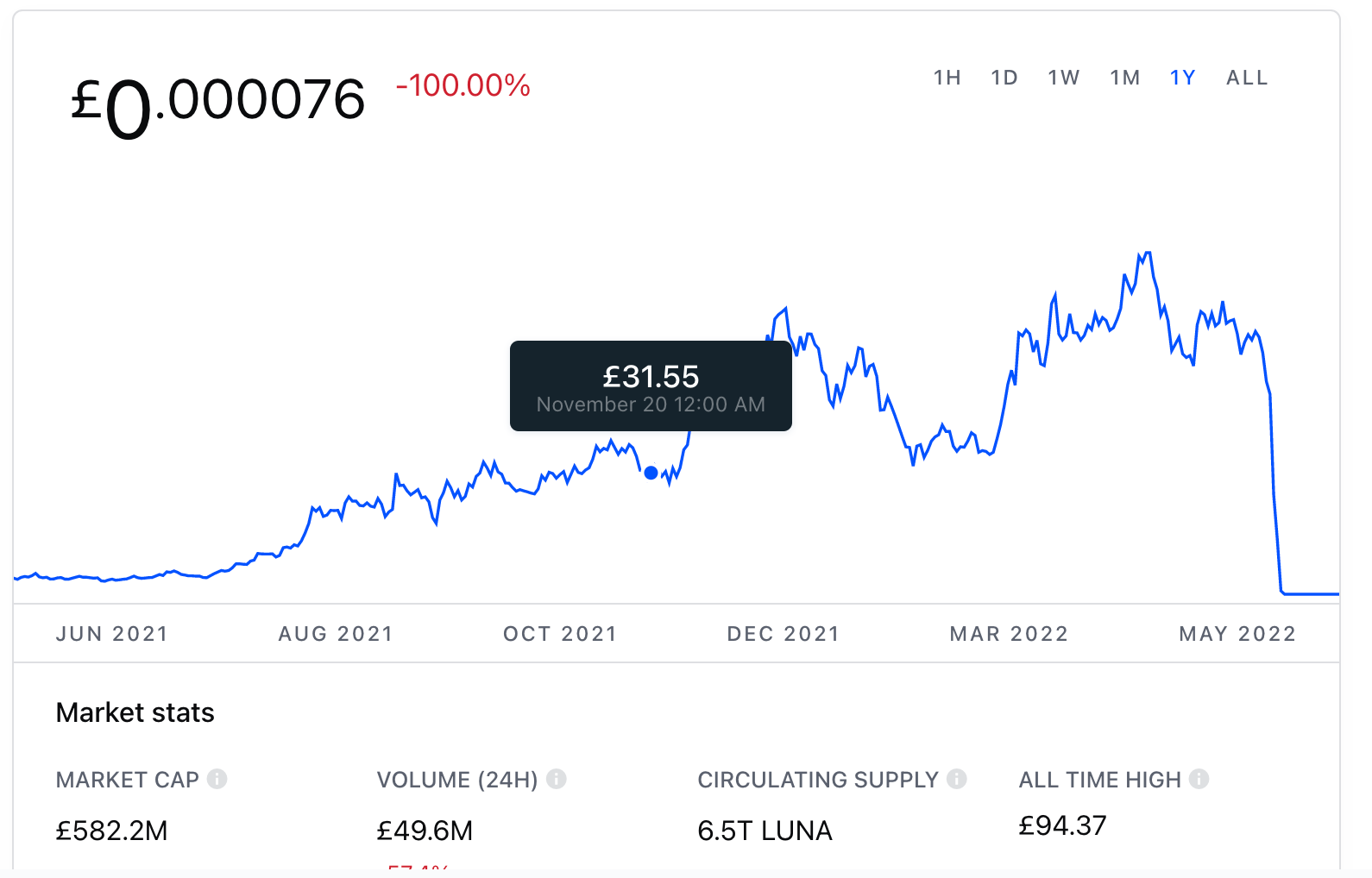

3 months is a long time in cryptoland. For the uninitiated, Terra and Luna might sound like somebody's pet cats. But together these two so-called 'Stablecoins' recently lost $50bn of value in 3 days. The irony is of course that a stablecoin is a specific type of crypto currency that has been designed to resist the volatility of typical cryptocurrencies.

Stablecoins were created to act as a bulwark against the price volatility of typical crypto currencies - Bitcoin being a good example of a volatile cryptocurrency. A Stablecoin is a cryptocurrency whose value is pegged to fiat money. Stablecoins work in 3 ways (1) they are asset backed - i.e. the issuer holds an equal amount of fiat currency or precious metals. Tether is an example of this. (2) they are backed by a reserve of other cryptocurrencies. The Dai stablecoin for example is backed by a holding of Etherium and other cryptocurrencies. (3) they are algorithmically managed - with Terra being a good example. The algorithm controls the supply of coins, keeping the price more or less constant. A lot of crypto investors use stable coins as a means of payment to reduce the exposure to the inherent volatility.

Terra is an algorithmic stablecoin whose price is theoretically kept stable by algorithmically increasing or decreasing the number of Luna coins in circulation, with a fixed exchange rate between Luna and Terra. However this has proven to be fallible with both losing the majority of their value recently. The jury is still out as to whether we are seeing a slow run on Tether as we speak, despite the very stringent conditions for converting Tether into fiat money.

So what does this mean for crypto, and Decentralised Finance (DeFI)?

Arguably, one of humankind's greatest inventions is money. As Yuval Harari notes, money is one of the most universal enablers of human collaboration, and one of the reasons that two people who have never before met, can transact with each other. In Harari's words: "Money is more open-minded than language, state laws, cultural codes, religious beliefs and social habits. Money is the only trust system created by humans that can bridge almost any cultural gap, and that does not discriminate on the basis of religion, gender, race, age or sexual orientation. Thanks to money, even people who don’t know each other and don’t trust each other can nevertheless cooperate effectively." (Yuval Harari, Sapiens)

Money has had an interesting journey from the days of shells and shiny objects, through to promissory notes, coins, paper money, and ultimately to fiat money. Along the way, the value of money has gotten more and more abstract. Originally the value of money was captured in the currency - as in gold and silver, copper or bronze coins. With cash came the bankers promise, but money was still pegged to precious metal - gold reserves. In recent times fiat money has moved away from the idea of pegged value, so it has achieved the state which Harari describes as inter-subjective reality: when a community of people agree to believe something and assign value to something that doesn't physically exist. Like a national border, or a law, or in our case the idea that a printed piece of paper has an intrinsic value of £50, because it says so, and because this ultimately has the backing of the government. Even if we switched to digital money in this manner, we would still be dealing in Pounds and Dollars, and the money supply and monetary policies would be defined by the government and the central banks. (Jack Weatherford's excellent book on the History of Money is a great read, by the way)

That brings us nicely onto the notion of Decentralized Finance (DeFi), an alluring, if somewhat unclear term. The Financial Policy Committee (FPC) of the Bank of England have defined DeFi as "...a set of alternative financial markets and products built on distributed ledger technology". In a 2022 report, the FPC identify that the DeFi market (total investment) is $180bn in 2022, which is a 5x growth from a year ago. Note that financial products and markets here goes beyond crytpocurrencies, to lending, asset management, derivatives, and insurance. The 40 page report does a great job of highlighting the various risks involved in DeFi. Some of those risks have proved to be all too real in the past couple of weeks as the value of many crypto assets have nosedived.

Putting aside the crypto and stable coin volatility, let's take a closet look at DeFi. The attraction of DeFi stems from the promise of freeing the world from the clutches of the stereotypically evil banking system. But is this really the case? The decentralisation in DeFi often refers to the disintermediation of the central or reserve bank rather than the private financial institutions. And as recent history suggests, the alternative to a central bank should neither be a a fallible algorithm, nor an anonymous and opaque private entity. Who controls monetary policy in a DeFi environment? Is decentralised really a euphemism for unregulated?

A second implication of DeFi is the disintermediation of the global payment infrastructure providers, and the creation of a faster and more efficient payment environment. The FPC report notes these advantages. There's definitely potential here, but again, we need to distinguish here between an enabling technology (distributed ledgers) and a currency (crypto-coins). To improve payments, the former is key, but the latter should be optional.

A third implication of DeFi is actually within organisations and smaller ecosystems and the extension of the distributed ledger technology to other forms of financial products such as mortgages, loans, and insurance. Once again, there's a benefit of using an emergent and more efficient technology, versus conflating it with the use of cryptocurrencies.

There's a rallying call you hear when it comes to decentralised finance - about building a better system that will get us out of the clutches of the big bad banks who have been in power for a long time. But look closely at the ownership and governance of the major cryptocurrencies and exchanges. We know Bitcoin was founded by the mythical Satoshi Nakamoto (mythical because his real identity is as yet unknown). Nakamoto has handed over the code and governance of Bitcoin to the community, but still owns around a million bitcoins which makes him among the top 20 richest persons in the world. Bitcoin's governance is embedded in code, which makes it somewhat democratic but also incredibly complex with philosophical debates around trustless networks at the heart of the governance debates. Ethereum has a similarly complex governance structure defined by its various stakeholders - which include nodes, exchanges, traders, developers, and more. But then you get to others such as Terra/ Luna which are owned by an individual - Do Kwon, who runs the company Terraform Labs, which like a lot of crypto players is shrouded in mystery. According to Crunchbase, Terra has just 5 employees. Do Kwon has also failed with previous Stable Coins. Binance, a leading Crypto exchange is owned by a billionaire developer, Changpeng Zhao, which is registered in the Cayman islands. Binance is under investigation by the US and UK governments and was ordered to stop trading in the UK in 2021. Also in 2021, Binance allegedly shared client data including names and addresses with the Russian Government (which Binance denies).

So depending on your level of crypto optimisim/ pessimism, Decentralised Finance is either a new world waiting to happen, with a number of expected missteps that are essential to the creation of a new order, or it's a wild west get rich quick ponzi scheme playground with any number of private investors with vested interests, operating on the edge of legal and regulatory environments.

Personally, I wonder whether we assign arbitrary value to the idea of decentralisation based on our declining in trust in authorities, without perhaps understanding the implications of such decentralisation. Much like another similar idea - holacracies - it's allure lies more in theory than in implementation. And maybe decentralization in a lot of these scenarios actually a ‘re-centralization’ - just with a different entity at the centre.

Also read:

The Moral Case Against Crypto (FT)

The Bank of England Paper on New Forms of Digital Money

The Bank of England letter to all CEOs of Financial Institutions about Crypto-exposure

The report from the Financial Stability Board (FSB) on Risks to Financial Stability from Crypto-assets

Other Reading This Fortnight

(1) EDF launches innovation strategy based on Blockchain and AI. (Power-Technology.com)

(2) How transport systems should evolve with changing travel patterns (Economist)

(3) Royal Mail’s delivery drones serve far flung places (IEEE Spectrum)

(4) Block is Jack Dorsey’s ecosystem start up spanning Square, Tidal, CashApp, and many others (Block)

Our Healthcare Event With The HSE

Last week we had the privilege of hosting the HSE’s (Health Services Executive, Ireland) Digital Academy Forum event at our Letterkenny Global Delivery Centre. It was a day of listening to inspiring stories of innovation in Healthcare and a glimpse of the future. Healthcare will be connected, predictive, data driven, and transformed over the next decade.

Have a great week!