#225: Strategy Needs Innovation

Strategy, Innovation, and Learning need to be tightly intertwined, for great outcomes.

Paul and Gary Donovan are brothers. But not just any brothers. They won an olympic silver medal in rowing in 2016. And when they were asked about their ‘strategy’ - they famously said you just have to “… close your eyes and pull like a dog”, which became a meme for a while. The point was, you don’t need much of a strategy for something so straightforward.

Suppose I show you a staircase and ask you what your strategy is, to get to the top. You might think me a bit strange or wonder what I’m talking about. But now imagine that I tell you that one of the steps (you don’t know which one) is an exploding step. Now you need a strategy. What will minimise your risk? Taking big strides to touch the minimum number of steps perhaps?

What is strategy?

A significant percentage of management literature is devoted to strategy. Perhaps one of the greatest thinkers about strategy is Michael Porter. He says in his 1996 HBR article that operational efficiency is not strategy, and that delivering efficiency is necessary but not enough. Strategy comes from a set of unique activities, and relies on choosing to perform activities differently from rivals. Such an approach usually requires tradeoffs - and the choice making is critical to strategy. Strategy critically involves choosing what not to do. And in Porter’s view, the level of fit between strategy and operating efficiency drives sustainable competitive advantage. Henry Mintzberg another well known commentator on strategy, also makes the point that strategy is often confused with planning. In Mintzbergs view, strategy is a creative exercise, while planning is an operational one.

Which brings us back to the point about the exploding steps. You usually need a strategy when faced with a challenge, and a complexity. This is why consulting firms such as McKinsey have historically used the SCQA framework. (Situation, Complication, Question, Answer) It forces you to frame the complication and the key question to be answered. You don’t need a strategy to climb a flight of stairs, but you might need one if it was a flight of 10,000 stairs, or a competition, or there were hidden dangers. Businesses are faced with complications all the time - from the competition, customers, suppliers, and environments, so the need for a strategy is a given.

But something is happening that adds another twist. We are now definitely in a cruel world. The idea, articulated in David Epstein’s book, “Range”, suggests that the pace of change makes past experience inadequate in shaping the future strategies. The world has always been changing and you could argue that even during the industrial revolution there was concurrent change of production, information, and communication technologies. But a tipping point has now been reached where significant change is taking place within timescales that are less than typical business cycles - i.e. the time to construct and execute a business strategy - say 3-5 years. To put it in today’s context, a strategy formulated 5 years ago may not have taken into consideration the covid pandemic, the Ukraine war, the Palestinian conflict, generative (or other) AI, the growth of robots, autonomous vehicles, or EVs… you get the idea.

Which means that even the idea of strategy as articulated by Porter or Mintzberg would be necessary but not sufficient. Whatever your strategy, you would face an execution landscape that was changing in ways that your strategy did not consider. In some ways this is not a new problem. When we set out to run a project 5 years ago to use sensors to help keep elderly people safe in their homes, we thought we had a great strategy and the right partners. We had a city council, a national healthcare organisation, and a university. We had partners for sensors, cloud, communication, and a platform that would deliver. Setting up 20 homes seemed like an easy task. Then we ran into the pandemic, the national healthcare organisation had a major cyber attack, there was an incident of a homicide at the set of homes we had identified, and to top it all, the frontline council workers refused to participate in the program.

By the way, this is a very good point to remind ourselves of the Anna Karenina principle. The famous novel by Tolstoy opens with the line “Happy families are all alike; every unhappy family is unhappy in its own way”. As a business principle, it means that there are many ways to fail, any one of dozens of things could cause your strategy or your project to fail. But the path to success is narrow and involves getting all of them right. It’s a very apposite idea for the challenge of converting strategy into successful execution, made more complex by the changing world.

What is innovation?

Just as with strategy, you can fill a library with books and articles about innovation. Most innovation definitions rest on 2 pillars. The first is the idea of doing something new - new to the world, new to your industry, or just new to your business; and the second is the implicit assumption that this will improve your business. It could improve your topline, reduce your costs, make things faster, improve customer experience, drive stakeholder value, benefit your community, or something else beyond this list.

The bottom line is that the cruel world - the fast changing, constantly challenging environment - needs us to increasingly do new things at a speed that we haven’t had to before. You might have had a strategy for your customer service or contact centre but now you’re having to rapidly adopt generative AI in that space. Or perhaps your supply chain strategy is requiring constant rethinks based on the conflicts across the world.

Innovation is therefore also the methodology and the capability to experiment and test and learn efficiently so that these changes can be effectively incorporated into your business, making your organisation as well as your strategy agile. Innovation involves a constant scanning of the environment to pick up change signals, maintaining a portfolio of ideas as a response to the environment change, which will keep your strategy on track, and an execution model that focuses on learning by doing, running controlled experiments, and scaling effectively.

My argument here, therefore is that you absolutely need a strategy, to make the big choices, but it’s not enough. You need to couple strategy with innovation to enable the change quotient. In fact, innovation even has a role in strategy formulation. For many large organisations, the strategy process itself takes months, and involves gathering data, reviewing options and making those big calls between alternatives. Maybe its about market segments, or supply chain set up, or your product mix, or even about your operating model. I believe that in our ‘cruel world’, an innovation strand, or a rapid test and learn cycle should be embedded into your strategy model, and conversely, your strategy should also be more agile and iterative. Nothing sets of warning lights as much as when I hear somebody says ‘this is an interesting idea, but it doesn’t fit with our 3 year / 5 year model, and we’re only 18 months into executing that plan’.

A Combined Model:

So what does a combined model look like? I call this an agile strategy model:

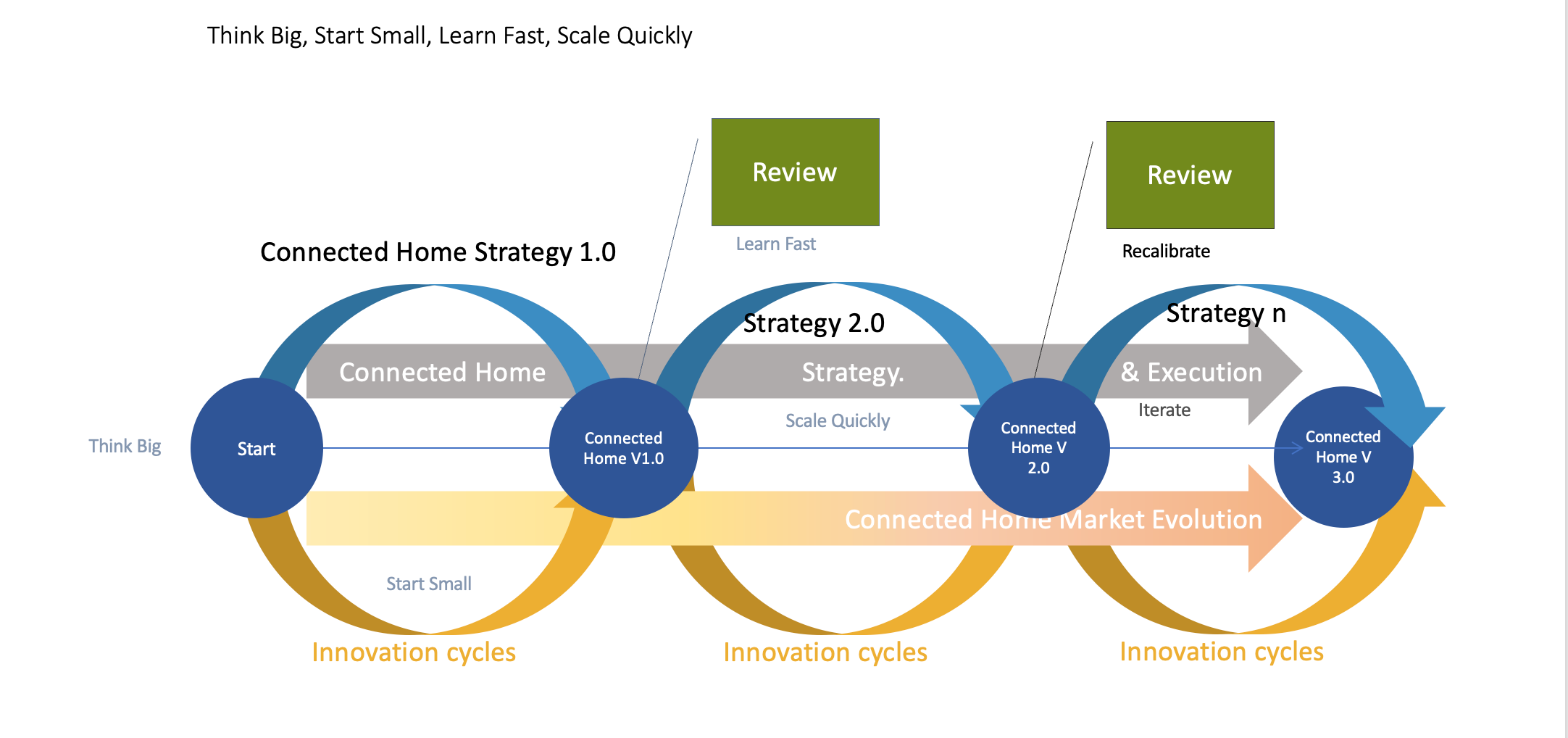

Let’s suppose you’re building a strategy for a connected home proposition. You might be a utility company, a consumer electronics business, a healthcare company, or a technology business. This is how it looks typically.

But in reality, the market is evolving quickly so it might have changed significantly from the time you build your strategy to the time you start to execute.

So there’s a good chance your strategy is very quickly outdated. The adaptive strategy model would look more like this. Instead of distinct think and act phases, the thinking and acting are both cyclical. The thinking never really goes away.

But this too is missing a piece. No matter how deeply you think, there’s always going to be the execution challenges and points where your assumptions don’t bear up to market realities, or the previous market realities are no longer valid. So what this piece needs an accompanying innovation cycle.

As you can see this is the classic think big, start small, learn fast, scale quickly model that lean start ups follow, but it is equally accessible to large firms, if you can blend strategy and innovation.

In reality, the innovation cycles could be much smaller, so it may look more like this.

In sum: this model addresses 2 challenges. There is the classic gap between the assumptions that your strategy rests on, and the reality on the ground. In our example of healthcare and connected home, our strategy did not factor in that the frontline workers would oppose the idea even though in our understanding it made their lives easier. They perceived a liability which we hadn’t quite understood, despite speaking with them beforehand. The second gap is the challenge of the fast changing environment. A strategy that takes 6 months to pull together is more than likely to be out of date given the rate of technology change at present.

There are 2 ways to look at our experience with the healthcare project. You could argue that we struggled to execute our plan. On the other hand, a typical project like that might have wasted many millions of pounds and euros if we had gone down the traditional model of strategy, lined up a full scale supply chain and execution model, and then discovered the problem. This is innovation doing its job, and building a learning engine that informs the strategy.

AI Reading

Overheated: This piece suggests that the AI market is overheated / overrated / losing steam, and that many AI businesses won’t make it through and the productivity benefits aren’t quite stacking up yet. I think there’s some truth in this but it still feels too early to call it.(WSJ).

Overpromised: It seems like a lot of the recent AI announcements from Google and OpenAI were the result of competitors falling over themselves to make announcements before the products were ready. This article says GPT4o is also a disappointment. (WSJ)

Criminalized: Criminlas are finding more and more ways to use AI. From beating KYC systems, to deep fake voices, there’s a growing list of ways in which AI is being put to harm. (MIT Tech Review)

Under-prepared: This piece from McKinsey on the other hand argues that the collective impact of AI and other changes will lead to 30% all current productive hours to be automated by 2030. And that there will be significant skill shortage in new areas. The idea of looking AI and automation at a task and hours level rather than people and jobs makes a lot more sense to me. (McKinsey)

Embedded: IDC looks at all the areas where AI will go under the hood - in semiconductors, in servers, in devices, and smartphones. (IDC)

Lives Changed: ultimately, you can look at macro numbers, or you can look at individual transformation stories. There are currently people whose lives are being transformed by Chatbots - as they deal with dyslexia, dyspraxia, ADHD, and other challenges. (BBC)

Other Reading

Upskilling: The coming challenge - not just tech but even declining interpersonal skills, according to this report (FT)

Deepfake Hack: Apparently an employee from Arup was duped into paying the equivalent of £20m to miscreants based on an AI generated deepfake call. (Guardian)

Science/Fiction: this is a great newsletter about scientific fraud, erroneous studies, and retracted research. Including somebody who has some kind of record for the most number of papers retracted - 210! (Science Fictions on Substack)

Sports/ Neuroscience: the latest thing in performance management - how neuroscience is behind better answers to ‘muscle memory’ and the proverbial ‘arm around the shoulder’, amongst other areas. (Guardian)

Quantum/Chemistry: how quantum computing is starting to impact practical chemistry in the real world. (Science.org)